“The aging and decreasing population is a serious problem in many developed countries today. In Japan’s case, these demographic changes are taking place at a more rapid pace than any other country has ever experienced.” – Toshihiko Fukui, the 29th Governor of the Bank of Japan

“I have experienced failure as a politician and for that very reason, I am ready to give everything for Japan.” – Shinzo Abe

“Here is the reality of Japan’s demographic crisis: at eight births per 1,000 people, Japan’s birthrate in 2013 was among the lowest in the world. Meanwhile, the proportion of the population over 65 is now 25%, the highest in the world. In 2010, Japan’s population peaked at 128 million. Current projections show the population dropping below 100 million by 2048 and as low as 61 million by 2085. The country’s working-age population has been declining since the late 1990s, making it increasingly difficult to care for Japan’s retirees.” – Saskawa Peace Foundation USA

Japanese stocks are breaking out (have broken out?). Irrespective of which measure of market performance you prefer, the TOPIX or the Nikkei, the recent performance of Japanese stocks has been impressive. And, if you are wondering, it is not because of a weakening yen.

Tokyo Stock Price Index (TOPIX)

Source: Bloomberg

Nikkei 225 Index

Source: Bloomberg

Japan’s demographic challenge is well-documented. More than a quarter of the population are 65 years old or older. Birth rates are at record lows. And since one of the market truths many of us have come to know and accept is that “demography is destiny”, we know that Japan’s economy will only continue to struggle. With the prevalence of this type of thinking, it is no surprise that many have been confounded by the recent rally in Japanese stocks.

Channelling our inner Charlie Munger we inverted and asked ourselves: under what scenario would Japanese-style demographics be the precursor to an economic boom? In our attempts to answer this question we have to come to the conclusion that the Japanese economy is quite possibly on the cusp of a virtuous growth cycle because of demographics not in spite of them.

We arrived at this conclusion due to one simple reason, we think that the Japanese economy is well-placed to lead and reap the benefits of the coming robotics revolution. Concurrently, Japan’s demographic challenge means, while the country is not entirely immune, it is uniquely sheltered from the potentially negative socio-economic consequences that may arise from the increased proliferation of robotics and artificial intelligence. (We have previously articulated some of our concerns around the unbridled development of artificial intelligence in Artificial Intelligence and Meaningful Work.)

Unemployment is low. Labour force participation levels are high. The overall population is declining while the elderly population is increasing and the labour force dwindling. Corporates are hoarding cash – companies listed on the Tokyo Stock Exchange just set a new record –their cash holdings are now more than 140 per cent of Japan’s GDP. The enormity of the level of cash holdings is better appreciated when compared to the 43 per cent of US GDP equivalent held in cash by US corporations – this 43 per cent includes the much talked about cash held offshore by the likes of Apple and Microsoft.

Japanese Unemployment Rate (%)

Source: Bloomberg

Japanese Labour Participation Rate (%)

Source: Ministry of Internal Affairs and Communications

The confluence of all these factors makes Japan ripe for the uptake of robotics to really accelerate but for one missing ingredient: capital investment. Although there is some evidence of capital investment picking up, Japanese companies have continued to demonstrate high levels of restraint when it comes to capital spending.

Despite the investment restraint shown by corporations, necessity, invention and a focused robotics strategy introduced by the government in 2015 – New Robot Strategy – has already positioned Japan at the forefront of the robotics revolution. We think there are a number of factors that will push Japanese corporations towards increasing capital investment and lead them to aggressively adopting robotics and artificial intelligence.

During the campaigning for the recent elections, opposition leader Yuriko Koike – governor of Tokyo and former Minister of Defense – called for a punitive tax on corporate cash reserves in order to encourage companies to invest more. While Koike’s new Party of Hope was resoundingly thumped by Prime Minster Abe’s Liberal Democratic Party (LDP), Koike’s criticism of corporate cash hoards resonated with members of the LDP. The government of Japan, we expect, will exert increasing amounts of pressure on companies to force them into spending their cash piles by increasing capital investment and paying higher wages.

When President Trump came into office he promised to shake up global trade in order to put America first and cut the US trade deficit. He brought in global trade hawks – Secretary of Commerce Wilbur Ross, Director of the White House National Trade Council Peter Navarro, and Trade Representative Robert Lighthizer – to form part of his administration. To date, very little of note has been achieved by the Trump administration on the trade front. With Trump also having failed to deliver on the domestic policy front, however, we think he will seek to overcompensate by taking a more aggressive stance on US trade policies. Especially as the president has the power to levy trade tariffs on countries without needing approval from Congress. More importantly for Japan, however, we think the Trump administration is also likely to become more aggressive in calling out countries they deem to be “currency manipulators”. And with the yen significantly undervalued in terms of its real effective exchange rate, there is little room for the Bank of Japan to talk down the yen. Moving forward, Japanese companies are unlikely to be able to rely on an undervalued currency to drive exports. Quality and sophistication – two traits that have traditionally been the hallmarks of Japanese products – will have to come to the fore. And that requires capital investment and potentially re-shoring of some manufacturing capabilities back to Japan.

The Chinese government’s strategic plans are progressively more focused on increasing local consumption and having much more of its population employed in higher-paid positions. This requires Chinese businesses to move up the value chain. And it is in response to such government objectives that industrial companies in China have started to move into the production of higher-value added goods – venturing into territories normally occupied by Japanese companies. As the threat from China intensifies, Japanese industrials will have to respond by increasing the complexity and quality gap between them and the competition. The Japanese, however, do not have the luxury to call upon a deep pool of labour. They instead will have to invest in robotics and automation if they are to have a chance of staving off the Chinese threat.

Given all the above factors, we think it is not a question of if but when Japanese companies will start increasing capital investment. And we think that the time has come.

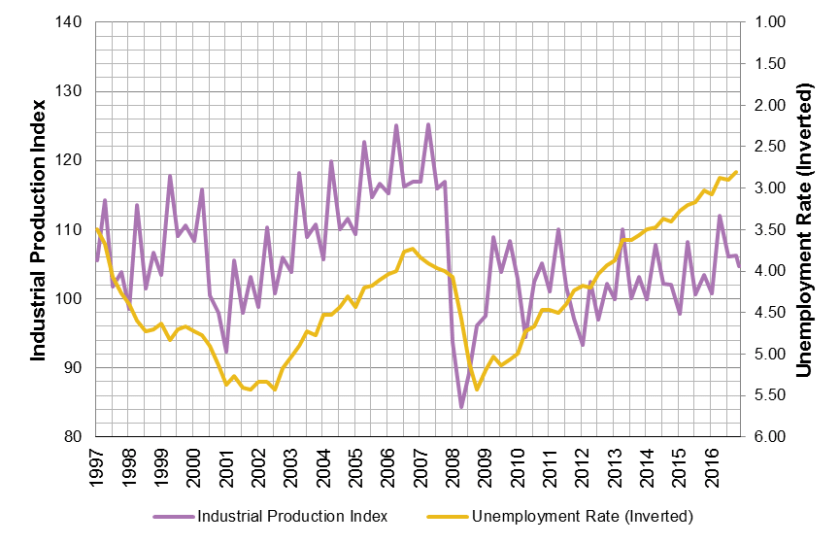

Japanese Industrial Production vs. the Unemployment Rate Sources: Ministry of Economy Trade and Industry, Bloomberg

Sources: Ministry of Economy Trade and Industry, Bloomberg

Investment Perspective

Corporate profits as a share of GDP, in Japan, are making new highs. Higher profits combined with high levels of cash and low levels of leverage encourage companies to undertake capital expenditures. Capital expenditures increase private sector profits and create demand for credit to the benefit of banks. Et voilà, a virtuous economic cycle.

Japan Credit to Private Non-Financials (% of GDP) vs. TOPIX Index

Sources: Bank for International Settlements, Bloomberg

While not so simple, Japan indeed is on the cusp of a virtuous private sector profit cycle. So the question to our minds is not whether one should have an allocation to Japan or not but rather should the allocation be currency hedged or not. And to do that we say, ignore those calling for the yen to 200 and do not hedge. On a real effective exchange rate basis, the yen is significantly undervalued.

Japanese Yen Real Effective Exchange Rate

Source: Bank for International Settlements

While this is a broad market call, we do want to highlight two sectors – one to overweight and the other to avoid. One of the sectors we are most bullish on in Japan is the healthcare equipment and services sector comprising of companies such as Olympus Corporation and Terumo Corporation. Japan is at the forefront of elderly patient care – its population has the longest average lifespan in the world. Healthcare equipment and services providers in Japan have supported the Japanese healthcare sector in facing the challenges posed by a rapidly aging population by delivering cutting edge solutions. As the US and Europe increasingly face up to the demographic challenges Japan has already gone through, there is an inevitable opportunity for Japanese healthcare equipment and service providers to increase their global reach and grow their exports to the US and Europe.

The one sector that we prefer to avoid in Japan is the financial sector. If a capital investment cycle kicks-off in Japan, as we expect it to, Japanese companies do not need to borrow – they are already sitting on so much cash – and this perhaps means that this spending will not automatically lead to an increase in demand for credit and nor does it imply that a meaningful rise in interest rates will be forthcoming.

We are long the iShares MSCI Japan ETF ($EWJ) as well as a select number of healthcare equipment and services providers.

This post should not be considered as investment advice or a recommendation to purchase any particular security, strategy or investment product. References to specific securities and issuers are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed.

“And, if you are wondering, it is not because of a weakening yen.”

How about the 6Trn Yen ETF buying from the BOJ?