“Good governance with good intentions is the hallmark of our government. Implementation with integrity is our core passion.” ― Narendra Modi, current Prime Minister of India

From the Wall Street Journal:

“India, the world’s biggest untapped digital market, has suddenly become a much tougher slog for American and other international players.

Over the past year, Indian policy makers have begun erecting roadblocks through special requirements for how U.S. tech companies structure their operations and handle data collected from Indian customers, according to industry executives and experts following the market.

Seeking to match China’s success at protecting and promoting homegrown tech giants, such as Alibaba Group Holding Ltd., Tencent Holdings Ltd. and TikTok parent Bytedance Inc., India is increasingly trying to shelter domestic companies. In the crosshairs, beyond Walmart, are firms including Amazon.com Inc., Alphabet Inc. ’s Google and Facebook Inc. and its WhatsApp messaging service.

Indian officials say they have an array of aims: protect small bricks-and-mortar businesses, secure user data and allow room for India’s own tech firms to grow. That smacks of protectionism to Western tech executives, who say India’s goals make it difficult to predict business conditions.”

The best laid plans of mice and men often go awry.

Investing in emerging markets is fraught with risk. Moral hazard and fluid regulatory regimes, means unsystematic risk cannot be easily diversified away, especially by foreign investors.

On to the update.

Change is Afoot: Fiscal Stimulus

Last week we commented that for markets to continue marching to higher levels there is a need for another catalyst. This week, we seem to have received the first hint what that may be.

Japan’s Prime minister Shinzo Abe has launched a new fiscal stimulus program with a larger-than-expected yen 13.2 trillion (US dollar 121 billion) package to repair typhoon damage, upgrade infrastructure and invest in new technologies.

According to the Financial Times, “the spending package is one of the largest since the 2008-09 financial crisis, as Japan seeks to fend off weakness in the global economy, drag from a recent rise in consumption tax and the risk of a slowdown after next summer’s Tokyo Olympics.”

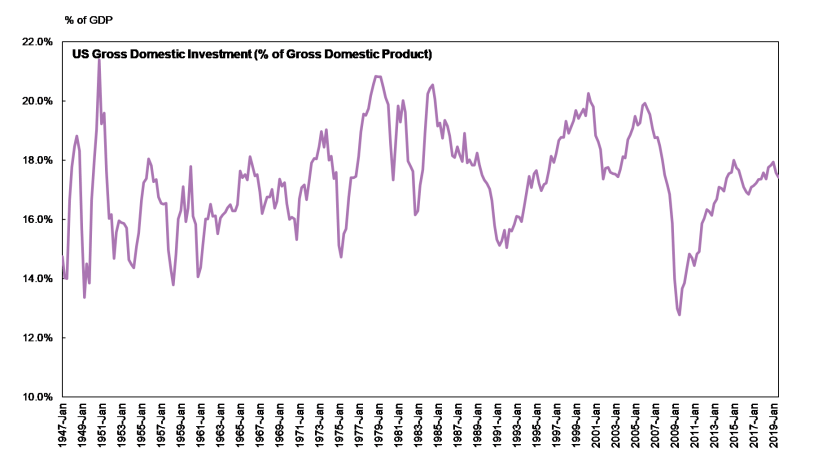

Since the Global Financial Crisis, despite loose monetary policy and record low interest rates, corporate spending in most major economies, as a share of GDP, has failed to reach pre-crisis levels. For example, the below is a chart of gross private investment in the US as a percentage of GDP.

Cyclically, US domestic investment peaked at the end of 2014 ― right after oil prices collapsed, sending shale companies into a tailspin and drastically slowing the pace of capital heading for the shale patch. Just as gross private domestic investment started picking up again in response to President Trump’s tax reforms, the Fed started tightening monetary policy by raising interest rates and shrinking its balance sheet. Meaning that the global economy remained deprived of the two engines of increasing capital investment and loose monetary policy in the US firing simultaneously.

The Fed has since famously reversed course by cutting rates and re-starting balance sheet expansion. Corporate spending, however, has not picked up.

Corporations do not like to invest in uncertain times and there has been plenty of uncertainty about. To continue with the US as an example, companies are still coming to terms with the impact of the trade dispute with China and at the same time facing the prospect of an Elizabeth Warren or Bernie Sander presidency ― both candidates running on platforms with socialist leaning policies and neither seeming in the mood to curry favours to big business.

With corporations unwilling to spend, governments need to take the lead. And Prime Minister Shinzo Abe’s announcement this week indicates that the powers that be in developed market economies are getting the message.

Europe, too, seems to be getting its act together. Governments, universities, EU institutions and a number of major corporations have joined forces in a new industrial policy drive that could become a blueprint for many other technologies and sectors. A fear of becoming an economic and industrial backwater in the face of US technological supremacy, growing trade protectionism and Chinese state capitalism, European leaders, despite facing much political criticism, have embraced a reinvigorated industrial policy as a tool to assert the continent’s technological independence and ensure its economic survival.

The next step for Europe is too see a coordinated effort towards a comprehensive fiscal policy and loosening of the purse strings. With discussions over the EU’s euro 1 trillion-plus Multiannual Financial Framework on going, there is still hope for Europe to follow Japan’s footsteps towards a looser fiscal policy.

If the US, Japan and Europe can pick up the slack from corporations and engage in loose fiscal policies in and around the same time, the longest economic expansion on record can get longer and global equity markets can head higher still.

The Importance of Fiscal Stimulus

Why is fiscal stimulus important? To answer that question, we turn to the Kalecki-Levy Profit Equation:

Corporate Profit = Investment + Dividends – Household Saving – Government Saving – ROW Saving

From Profits and the Future of American Society: A Dramatic New Perspective on Capitalism by S Jay Levy and David A. Levy:

“The effect of government saving on the profits of the consumer-goods sector is the same as the effect of household saving. Whether consumers themselves save or government acting as their “purchasing agent” saves, the money will not reach the consumer-goods sector. Thus, a government surplus, like personal saving, would be a negative source of profits.

In 1980, the government had a deficit; its outlays exceeded its receipts. In other words, the government borrowed. Thus, it added to the flow of funds into the consumer-goods sector; it contributed to the sector’s profits. A government deficit is always a positive source of consumer-goods-sector profits.”

Most developed market governments can create money directly. Giving them, at least theoretically, an infinite capacity to borrow and dissave. More importantly, governments do not, or at least should not, operate for their own wealth generation, rather they operate for the benefit of the populace. For this reason, in periods where the desire to save is high, and the desire to invest is low, governments must dissave by running deficits and be the propellant for their stalling economies.

Based on the above formula, we can see that government spending (or dissaving) increases corporate profits. Increasing corporate profits, generally, translate into increased employment, higher wages and increased liquidity. All factors that contribute positively to household wealth and should translate into rising equity prices.

This post should not be considered as investment advice or a recommendation to purchase any particular security, strategy or investment product. References to specific securities and issuers are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed.