Contents

Thoughts and Investment Ideas for 2020

Ideas

Summary

Energy

The Speculative Phase: Software Over Semiconductors

Playing the Strength in US Housing Demand

Founder Exodus: A Reduction in Existential Flexibility

USD

Thoughts

Summary

Macro Risks

Inflation is the Enemy

Valuations

US Treasury Yield Curve

Modern Monetary Theory

Books

Five We Have Read and Recommend

Five from Our 2020 Reading List

Thoughts and Investment Ideas for 2020

“Can you ask a new question? It’s the new questions that produce huge advances…”

― Why Model? by Joshua M. Epstein

“A reward-sensitive person is highly motivated to seek rewards―from a promotion to a lottery jackpot to an enjoyable evening out with friends. Reward sensitivity motivates us to pursue goals like sex and money, social status and influence. It prompts us to climb ladders and reach for faraway branches in order to gather life’s choicest fruits.

But sometimes we’re too sensitive to rewards. Reward sensitivity on overdrive gets people into all kinds of trouble. We can get so excited by the prospect of juicy prizes, like winning big in the stock market, that we take on outsized risks and ignore obvious warning signals.”

― Quiet: The Power of Introverts in a World That Can’t Stop Talking by Susan Cain

“Stock prices have reached what looks like a permanently high plateau.”

― Irving Fisher (1867 – 1947)

The last twelve months, and pretty much the entirety of the last decade, handsomely remunerated the reward-sensitive ― the risk-takers, the optimists, the dip-buyers, the trend-followers, the bitcoin HODLers ― and punished the sceptics, the value-conscious, the doomers and the gloomers, and the short-sellers, without prejudice.

The sceptics, and others of their ilk, are quick to remind of the cyclicality of markets even as they lick their bull-horned wounds. That, as surely as night follows day, the years of plenty will be followed by years of famine. That valuations matter.

They, the doubters, are, as history shows, not wrong. Markets are indeed cyclical. Valuations do matter, eventually. The record shows, claiming otherwise will surely find you embarrassed, if not immediately, most definitely in due course.

There is, however, a wrinkle in the cyclicality argument.

All finite, deterministic systems are guaranteed to cycle. Capital markets, however, are neither finite nor deterministic.

Finite systems, to paraphrase James P. Carse author of Finite and Infinite Games, are comprised of known participants, fixed rules and agreed upon objectives. Infinite systems or games, on the other hand, are defined by participants both known and unknown, changing rules and an objective to keep the system or game perpetuating.

Markets are an infinite system and market participants ― investors, traders, brokers, market makers, regulators, corporations and whoever else that may choose to participate ― are engaged in an infinite game. To survive in an infinite game, participants must adapt or die. It is this process of adaptation that allows the system to perpetuate but at the same time necessitates that neither the duration nor the form of any given market cycle can be known before the fact. Just because the average bull market may have lasted 7-years or ended within a certain time period following a yield curve inversion does not in any way imply that this or the next market cycle will follow the same pattern.

Market participants should not, nay cannot, simply rely on a passing understanding of market cycles. Rather, we must all continuously strive to better understand how the game and the participants are adapting so that we may have a better shot at positioning for that which lies ahead.

In this piece, we try to ask questions ― with a bit of luck, some different, if not entirely new, ones ― and share our thoughts and ideas that, we hope, will help you, the reader, better play the infinite game over the coming six to twelve months.

Note: Comparable pieces for 2018 and 2019 can be found here and here, respectively.

Ideas

Summary

- Energy: Long Chevron $CVX, National Oilwell Varco $NOV and Cactus Inc $WHD and avoid allocations to energy importing emerging markets

- Speculative Phase: Prefer software $IGV to semiconductors $SOXX in the US

- Founder Exodus: Avoid long positions in companies that have recently seen their founders exit such as Alphabet $GOOG, Under Armour $UAA, Chipotle $CMG and Alibaba $BABA

- USD: Below 95 on the US Dollar Index $DXY, short Australian dollar and New Zealand dollar

Energy

“Rise early, work hard, strike oil.” ― John Paul Getty

“Do not waste energy, make it useful.” ― Wilhelm Ostwald (1853 – 1932), winner of the Nobel Prize in Chemistry in 1909

Humans have been burning fossil fuels to generate electricity since 1882. Coincidentally, the first hydroelectric power plant also began operations in 1882. Fissioning uranium isotopes has been a source of electricity since 1956.

The technology to harness fossil fuels as a source of energy at scale has transformed everything from agriculture to industry, transportation to warfare, quality of life to the environment, and everything in-between. Fossil fuels remain the most concentrated and versatile source of energy that can be converted at affordable cost and high rates of efficiency into heat, light and motion.

The quest to harness alternative sources of energy at comparable levels of efficiency, cost and scale as to that of fossil fuels remains just that, a quest. Progress is being made and the political will to turn our collective backs on fossil fuels has never appeared stronger.

The rise of environmental, social and governance (ESG) criteria in investing, the US Democrats’ “Green New Deal” on climate mitigation, and the recent unveiling of the “European Green Deal”, are raising the cost of capital for the global energy sector. All the while, returns on invested capital being generated by the sector remain dismal.

The potential unintended consequence of a seemingly coordinated desire to penalise the global energy complex and starve it of fresh capital is the prospect of a negative energy supply shock becoming increasingly probable.

With the promises of blockbuster shale wells fracking companies made to investors turning out to be a busted flush ― according to The Wall Street Journal wells drilled recently in the four largest US oil regions were on track to produce nearly 10 per cent less oil and gas over their lifetimes than companies forecast ― and the sector facing ever increasing costs of capital, the prospects of a global energy supply shock in the near-to-medium term, we think, are under-priced.

Barring a negative-demand shock, or a breakthrough in technology that enables the harnessing of alternative sources of energy as efficiently and cost effectively as harnessing fossil fuels, we think oil prices can head higher, much higher, in the near- to medium-term.

We often use the 48-month moving average, for commodities and major currency crosses, to guide our trading strategy. For now, WTI crude prices remain above the moving average. As long as prices do not meaningfully breach the 48-month moving average, our bias is to be long in expectation of prices continuing to climb the ‘Wall of Worry’ over the next 6 to 12 months.

Tactical Perspective

President Trump’s decision to order the Iranian Major General Qasem Soleimani’s death via drone attack in Baghdad in the evening on 2 January saw oil prices spike by as much as 4 per cent. Such is the antipathy towards energy stocks that despite a sharply higher oil price, the SPDR Energy Select Sector ETF $XLE closed in the red on 3 January.

With that being said, oil may have to work off overbought conditions if and when the geopolitical risk premium subsides. We would hold off till that point to have a full-sized allocation to energy.

Ideas: Long Chevron Corporation $CVX, Long National Oilwell Varco Inc. $NOV, Long Cactus Inc. $WHD.

Avoid: Energy importing emerging markets.

The Speculative Phase: Software Over Semiconductors

If the US equity market is in the throes of a market melt-up, or an almighty blow-off, the rally should devolve into becoming increasingly speculative.

Last year, software stocks were leading the pack till around mid-year when, as the trade tensions between the US and China thawed, semiconductor stocks started climbing a wall of worry and ended the year at all-time highs. Software stocks were the laggards during the second-half of last year.

We think as the rubber of hope meets the road of financial performance semiconductors are likely to falter. Further, given the sensitivity of semiconductor stocks to the trade deal and with a phase one deal between the US and China more than priced in, it behoves the prudent investor to pare allocations to semiconductor stocks. Rather, as growth becomes precious once again, we think, investors are likely to turn to software afresh. And as software incumbents look for new ideas and business models, more than a few acquisitions are likely to be in the offing.

For now, in US equities, we prefer software to semiconductors.

Ideas: Long Manhattan Associates $MANH, Long Salesforce.com $CRM, Long Avalara $AVLR, Long Slack Technologies $WORK, Long iShares Expanded Tech-Software Sector ETF $IGV

Avoid: iShares PHLX Semiconductor ETF $SOXX

Playing the Strength in US Housing Demand

Falling long-term interest rates equate to more affordable housing and on a relative basis make the economics of owning a home better than of renting one. With US long rates having dropped sharply during the summer, US home purchases have picked up.

On an annual basis, sales in October increased 4.6 per month from the same month the previous year, marking the fourth straight month of year-over-year gains.

With homeowners in the US remaining in their homes thirteen years on average, five years longer than they did in 2010, and housing inventory estimated to be at an 11-year low, the surge in demand for housing is rippling through to increased applications for and issuance of building permits.

The thing about buying a home is that, once you have bought one, it comes a with a long list of mandatory and not-so-mandatory purchases. For this reason, US consumer durable goods spending tends to closely track home sales and housing permit issuance with a lag.

While demand for housing fluctuates with long-term interest rates, once a house has been bought the spending that follows it, will follow irrespective of the fluctuation in interest rates. This makes consumer durable plays, broadly the consumer discretionary sector, a less interest-rate sensitive means of gaining exposure to the robust demand for US housing.

Ideas: Long Floor and Décor $FND and conditional on high-levels of risk appetite small caps such as Bassett Furniture $BSET and Hooker Furniture $HOFT

Founder Exodus: A Reduction in Existential Flexibility

Simon Sinek in a talk about his book The Infinite Game shares an anecdote in which Steve Jobs was almost on a whim willing to pivot Apple Inc., despite the prospect of huge near-term losses, when faced with an existential crisis. He describes this ability to be “existential flexibility”.

Founders, in general, are more likely to have the strength of character and conviction to make the difficult decisions ― that is, existential flexibility ― than do managers. A number of prominent companies ― such as Google, Under Armour, Alibaba and Chipotle Mexican Grill to name a few ― have recently seen their founders step down.

With the business cycle long in the tooth and regulatory risks, particularly for technology companies, rising, we prefer to avoid investing in companies that have transitioned from founder CEOs to manager CEOs.

USD

Analysts, ourselves included, have spent an inordinate amount of time and energy in an attempt to ascertain the direction of an asset that has remained in a mind-numbingly narrow range. Such is the importance of the greenback, implicit or explicit, in any investment framework, however, that we would be remiss to not once again touch upon it.

Yield Differentials

We use Australia and New Zealand, given access to a longer history and better quality of data, and because they serve as good proxies for China and commodity producing emerging markets. The below charts show that on the 10-year government bond yield differential basis there is a strong case to be made for a stronger dollar relative to these currencies. (We also include Indonesia, despite the limited data, as a further example.)

From the Perspective of Select ‘Fragile’ Emerging Markets

The real trade-weighted dollar has posted a smaller advance since mid-2014 than the US Dollar Index $DXY, suggesting that the threat to the world from a stronger US dollar is not as great as is often hyped to be.

Below we share three charts of select emerging markets that suffered severe crises and saw their currencies plummet versus the US dollar in the 1990’s. Most of these countries are better placed to withstand a stronger US dollar than they were prior to the crises in the 1990’s and at the time of the ‘taper tantrum’ in 2013.

Note: Pre-crisis metrics for 1996 for all countries except India, for India we use 1990

While a stronger US dollar would be painful, it would not, we think be apocalyptic barring a a severe spike (10%+ in a matter of months).

Ideas: Using $DXY as the guidepost, long US dollar below 95 versus the Australian dollar and New Zealand dollar, given the low cost of carry.

Thoughts

Summary

- Macro Risks: Using rallies to reduce equity exposures tactically and increase bond allocations, take profits in European equities

- Inflation is the Enemy: Growth shocks and not inflation shocks are probably the bigger risk to diversified portfolios in the near-term

- Valuations: Gold is indicating equity market multiples have peaked

- US Yield Curve: Prefer steepeners and then the short-end of the curve

- Modern Monetary Theory: Probably not what you expect

Macro Risks

The chart above is of the 52-week moving average of the Citi Macro Risk Index. It is not the magnitude rather the direction of the risk index that acts as a cyclical indicator. (Rising line indicates increasing macro risks.)

With the risks that built up during the sell-off in the last quarter of 2018 and the recession fears that peaked in the summer of last year having been largely unwound, some caution is now warranted. We think equity rallies hereon should be used to gradually reduce allocations to leave powder dry for cyclically more opportune times to go on the offensive.

The chart above is the ratio of gold, in euros, to the Euro Area all shares index versus the differential between 10-year government bond yields of the ‘fragile’ European economies and Germany. (For the latter we use the average of the yields on Spanish, Portuguese and Italian 10-year bonds and subtract from it the yield on 10-year German bonds.)

The two series are a means of measuring sovereign, or break up, risk in Europe. Rising ratios imply rising sovereign risks and a rush towards the safe havens of gold and German debt. Recently, with gold having rallied and some form of Brexit related agreement forming, the two time-series have diverged. The yield differentials indicate a declining risk premium while the gold-to-shares ratio indicates a rising risk premium.

With the hard work to resolve Brexit still pending and the potential for a flare up in a trade spat with President Trump under-priced, we think there is more than a modicum of complacency on investors’ part with respect to risks in Europe. Profits should be taken on European equities.

Avoid: Shorting funding currencies, namely the euro, Swiss franc and Japanese yen, as they can rally sharply during risk-off periods

Inflation is the Enemy

Generally, the main macroeconomic risk factors that drive expected returns in equities and bonds are growth and inflation. With equity returns being most sensitive to growth and bonds to inflation.

Lower expected risk-adjusted returns in equities begin to be priced in when the economy is supply constrained and central banks are tightening monetary policy to lower nominal growth. This also tends to be the more inflationary phase of the business cycle with rising unit labour costs and valuation multiples at or near cycle highs. In contrast, higher expected returns begin to be priced in when the economy is operating below potential and central banks are easing monetary policy to prop-up nominal growth. This generally tends to be a disinflationary phase in the business cycle with unit labour costs falling and valuation multiples at or near cycle lows.

The chart above is of the trailing earnings yield (inverted price-to-earnings ratio) of US stocks and realised inflation rates. Theoretically, since stocks are real assets, changes in the rate of inflation should not have a meaningful impact on stock prices or valuation multiples. In practice, however, the principle does not hold. Historically, US earnings yields have been more closely related to the rate of inflation than to nominal or real bond yields.

A comparable relationship between inflation and earnings yields has also been found to exist in many other markets.

The expected risk-adjusted return in bonds also tends to be counter-cyclical. Specifically, policymakers are more prone to hiking policy rates when there is little to no slack in the economy and inflation pressures begin to emerge.

At a portfolio level, risk-adjusted returns of the portfolio also depend on the correlation of constituent assets over the course of the cycle. Economic theory has it that asset prices reflect the present value of future cash flows. Given that inflation determines the discount rate for both equities and bonds, it also tends to drive both assets in the same direction. At times when inflation shocks dominate, equities and bonds become positively correlated. While, since growth rates affect equities more than they do bonds, growth shocks dominating leads to bonds and equities being negatively correlated.

The chart above is of the US stocks-to-bond correlation and the 6-month rolling average of the annual rate of inflation, as measured by the consumer price index excluding shelter.

During the period from 1965 through to 1997, when inflation expectations experienced large swings, the stock-to-bond correlation was almost consistently positive. That is, changes in inflation expectations drove both stock and bond returns and during periods of equity market weakness bond allocations did not make up the difference. For example, in the sub-period between 1973 and 1981, during which there was a negative supply shock from the OPEC oil export embargo, multiple recessions, high unemployment rates and high inflation, equity market weakness coincided with poor bond market performance.

The time-series demonstrates how the correlation between equities and bonds is not static. The implication being that bond allocations do not always serve as a suitable diversifier for equity allocations. Rather, it is the prevailing market regime, as described above, that determines the efficacy of bond allocations to lower drawdowns and portfolio level volatility during equity market sell-offs.

As the chart shows, the last decade, as all of us already know, was characterised by low-growth, negative growth surprises and low-and-steady inflation. That is, a decade of negative correlation between bonds equities.

Asset Allocation

A strategic asset allocation framework, it then follows, should contain equity and bond exposure levels conditioned on the phases of the business cycle.

Upside inflationary shocks make traditional 60/40 and risk-parity like allocations suffer as bonds and equities sell-off concomitantly. While periods of benign inflation with the occasional growth shock are well-suited to portfolios diversifying equity exposures with heavy bond allocations.

According to our framework, however, the probability of a near-term inflationary shock remains low. Rather, we anticipate the risk of a near-term negative growth shock to be much higher than that of inflation sustainably surprising to the upside.

“The driving force for underlying profits is credit growth, and in the process the most conservative among institutions compromise standards and engage in practices that they would not have dared pursue a decade or two ago. The heroes of credit markets without a guardian are the daring―those who are ready and willing to exploit financial leverage, risk the loss of credit standing, and revel in the present casino-like atmosphere of the markets.”

― Interest Rates, the Markets and the New Financial World (1986) by Henry Kaufman

An example of growth remaining elusive comes from the Federal Reserve’s recent senior loan officer survey, which revealed that banks left commercial and industrial lending standards mostly unchanged amid weakening demand for credit.

Bonds, rather than commodities and other inflation hedges, remain, for the near-term, the most suitable hedge for equity allocations.

Ideas: Long Japanese Government Bonds and allocations overweight bonds relative to equities and commodities (excluding gold / precious metals)

Avoid: Treasury Inflation Protected Securities (TIPS)

Valuations

The chart above is of the S&P 500 Index expressed in terms of gold (in US dollars per Troy Ounce) versus the index’s cyclically adjusted price-to-earnings ratio (as calculated by Professor Robert Shiller).

While we use the CAPE to smooth out the effect of the Global Financial Crisis, using annual price-to-earnings multiples would convey the same message. In simple terms, the price of gold is inversely correlated to the price-to-earnings multiple of the index.

The price of the S&P 500 in terms of gold suggests that valuation multiples have peaked on a cyclical basis.

Ideas: Gold can serve as a hedge for equity market multiple-contraction

US Treasury Yield Curve

“During 1870-1910, the decades of dynamic expansion, German government bond yields were actually declining. German yields did not decline as far as did British, Dutch, and French yields but were low enough to suggest that the savings of the people were keeping up with the financing requirements of a fast-growing economy. Germany was enjoying the benefits of that mighty weapon, a smooth annual accrual of new savings seeking investment in interest bearing securities. In the years before 1914, German bond yields were similar to yields in the United States, another large and fast-growing nation during the period 1870-1914.”

― A History of Interest Rates by Sidney Homer (1864 – 1953) and Richard Sylla

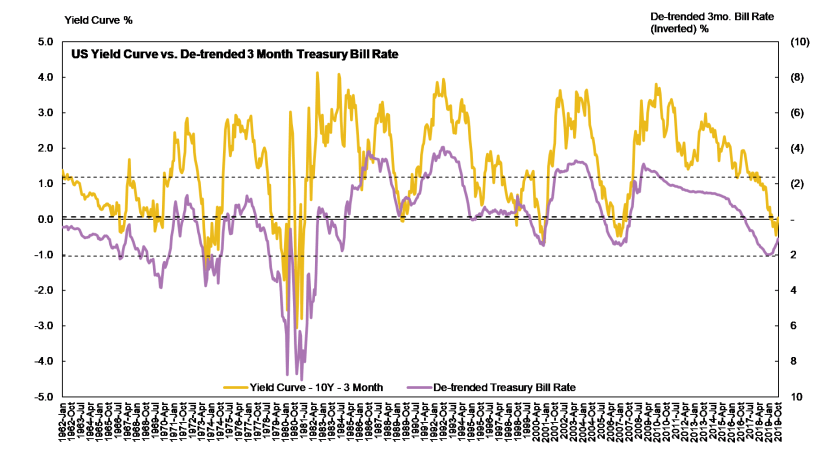

The chart below is of the US yield curve (10 year minus 3 month) versus private saving less private investment. The latter points towards a further steepening of the US yield curve.

The chart below is of the de-trended 3-month Treasury bill rate (inverted) ― de-trended by subtracting the 10-year moving average from the bill rate ― versus the US Treasury 10-year and 3-month yield curve. The chart dates from 1962 till today, suggesting that the de-trended 3-month Treasury bill rate contains information about the direction of the yield curve.

The two-time series have a correlation of -0.75 with an r-squared of 57 per cent.

(The dashed lines on the above chart are the average de-trended bill rate and levels one standard deviation above and below the average.)

The relation between the de-trended bill rate and the yield curve indicates a strong tendency of interest rates to mean revert. The wider the gap between the current de-trended bill rate and its long-term average, the stronger the markets expectation of mean-reversion.

This relationship, too, points towards a further steepening of the US yield curve.

Ideas: Long yield curve steepeners or alternatively long the short-end of the yield curve

Modern Monetary Theory

“‘War Board’ Proposed

April 13, 1933

A plan to mobilize private industry under the government for expansion in the production of articles and materials in normal demand, this expansion to be coeval with the administration’s public works activities, is being developed by the President’s closest advisors and they hope to persuade him to attempt it.

Certain types of industry, under the plan, would be assembled and regulated by a government agency reminiscent of the War Industries Board. Competition would be regulated: hours of work and minimum rates of pay would be fixed; and some of the proponents of the idea also would have the government guarantee manufacturers against loss in resuming or increasing the manufacture of prescribed articles and materials.

The thought behind the plan is that a public works program standing by itself, even if the five billions is expended upon it, will not sufficiently reduce unemployment or make use of the new purchasing power. It is contended that private industry must, at the same time, be put in a position to absorb the new purchasing power, composed of the billions which the government will be putting in the hands of citizens all over the United States. To do this, it must resume manufacture, and that will restore many to private employment in the factories themselves and in the retail establishments which will dispose of the products of these factories. This will, in turn, give purchasing power to those privately as well as those governmentally employed. A part of the billions will then flow back to the Treasury in various forms of taxation.

The argument which seems to have been most effective in bringing the administration to support the public works appropriations is that the deflationary policy has cut down the purchasing ability of the country by seven billions. Of this five billions is in closed banks, one billion in the budget savings and another billion in reductions made by the several State governments.

The vast public works program having been definitely agreed upon, with the probability that it may involve an expenditure of as much as five billions, it soon became evident to the architects of administration policy that this plan needed a companion.

It was all very well to balance the budget, and, with government credit thus establish, to borrow billions for roads, buildings, flood control and the like. But this question remained: How could private industry get the full use of those billions for purchase? Without some form of government stimulation and aid, it was felt that manufacturers of ordinary consumers’ commodities would wait to clear their stocks, while retailers were clearing theirs, and when the manufacturers did resume production, they would simply proceed at “depression pace.”

The result of these considerations was the plan to set up a government agency to induce industrial expansion, to quicken and regulate it meanwhile, to protect it against loss and perhaps even to fix the prices of labor’s product as well as the wage of labor itself.”

― In The Nation: 1932-1966, Arthur Krock (1886 – 1974)

Modern Monetary Theory (MMT) advocates fiscal measures and the role of government in the creation of money over monetary policy and as such stands in almost complete contrast to traditional macroeconomic theory. A key to understanding MMT is to appreciate the difference between users of currency, primarily the private sector, and the monopoly issuer of said currency, the government.

Beginning with the economic assumptions of full employment and full capacity utilisation ― that is, a country facing real resource constraints. Under such a scenario, inflationary pressures can become a genuine and immediate danger and monetary policy can, arguably, play a critical role play to dampen excess demand and by extension inflationary pressures. For instance, by raising the level of interest paid on excess reserves, the central bank could increase the opportunity cost of lending activities, encouraging banks to instead place more cash with the central bank or demand a higher rate of return from potential borrowers. Thereby raising the cost of capital.

Proponents of MMT contend that adjustments to the government’s fiscal policy could just as easily be used to achieve the same objective. For example, excess demand could be dampened by raising tax rates, be it income, sales or value-added taxes.

The reality today, however, is that few, if any, economies face resource constraints. Rather, interest rates persist at or near historic lows, inflationary pressures have remained transitory at best and the global commodity complex remains largely mired by excess capacity. Monetary policy has proven impotent in reflating the economy and zero-bound interest rates have neither spurred demand for credit nor compelled banks to lend.

In the current state of the global economy, MMTers argue, is when the prescriptions of the theory are most potent. Tax cuts, for example, can be utilised to immediately increase private sector disposable incomes.

By divvying up the economy across private and public sectors and recognising that the balance sheet constraints across the two sectors are incongruent, MMT perceives fiscal policy as a means to lessen (increase) private sector funding pressures, when the economy is operating below (at or above) capacity.

In a fiat currency system, the government has the flexibility to affect changes in private sector behaviour by fine-tuning its budget deficit. At a time when the private sector is deleveraging, if government fails to offset this by widening its budget deficit, it effectively starves private sector activity. In a fiat currency system, it is government, not the central bank, that creates new liabilities that become the assets of the private sector.

So, at any level of income, if the private sector decides to deleverage, the public sector must by definition, end up saving less by running a larger budget deficit or shrinking a budget surplus. In an ideal world, any shifts in the private sector’s propensity to save would be matched by an immediate change in the tax rate, and the combined income of the public and private sectors would remain stable. A key policy prescription stemming from MMT, then, is to keep monetary policy steady and to manage the economy by adjusting the tax rate.

The Practical Implications

Most discussions on MMT devolve into either how it spells the end of the US dollar, or fiat currencies in general, or how it will spur uncontrollable inflation and therefore one must own gold or bitcoin or both. With time these proclamations may prove correct. The thing about capital markets, however, is that for the most part it is the path not the endgame that matters.

And as far as the path is concerned, it is not unreasonable, in our opinion, that, initially, MMT, or any other form of government led fiscal activism, reinforces deflationary not inflationary forces. That is, by opening up the fiscal spigot policymakers continue to keep cost of capital artificially suppressed thereby further delaying the inevitable impairment of excess capacities, zombie companies and unproductive debts. Ever increasing advantages would then continue to accrue to large companies, with access to low cost capital, at the expense of small and medium enterprises, further compounding the issues of inequality and declining productivity. Such a deflationary death spiral is what, we think, precipitates the endgame, not a sudden burst of inflation.

Books

Five We Have Read and Recommend

- Surfing the Edge of Chaos: The Laws of Nature and the New Laws of Business by Richard Pascale, Mark Milleman and Linda Gioja

- The Match King: Ivar Kreuger, The Financial Genius Behind a Century of Wall Street Scandals by Frank Partnoy

- The Man Who Solved the Market: How Jim Simons Launched the Quant Revolution by Gregory Zuckerman

- The Great Rebalancing: Trade, Conflict, and the Perilous Road Ahead for the World Economy by Michael Pettis

- How Global Currencies Work: Past, Present, and the Future by Barry Eichengreen, Arnaud Mehl, and Livia Chitu

Five from Our 2020 Reading List

- The Education of a Speculator by Victor Niederhoffer

- The Model Thinker: What You Need to Know to Make Data Work for You by Scott E. Page

- Micromotives and Macrobehavior by Thomas C. Schelling

- Clash of Empires: Currencies and Power in a Multipolar World by Charles Gave & Louis-Vincent Gave

- Energy and Civilization: A History by Vaclav Smil

Thank you for reading and please share!

This document should not be considered as investment advice or a recommendation to purchase any particular security, strategy or investment product. References to specific securities and issuers are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed.